Although November got off to a sluggish start as traders and investors paused to reflect upon October’s sizable move and gains, the month ultimately succeeded in living up to its midterm-year reputation for solid gains. When trading ended in a dull half-day post-Thanksgiving-Day session, DJIA had advanced 2.5%, S&P 500 2.7% and NASDAQ 3.8% for the month. This performance was just slightly less than the average midterm November since 1950. Only the Russell 2000 small-cap index failed to live up to historical standards as it fell 0.02% in November compared to an average midterm November gain of 3.9% since 1982. Once again, DJIA, S&P 500 and NASDAQ all traded at new highs in the month. Russell 2000 has yet to eclipse its closing high from earlier this year in March.

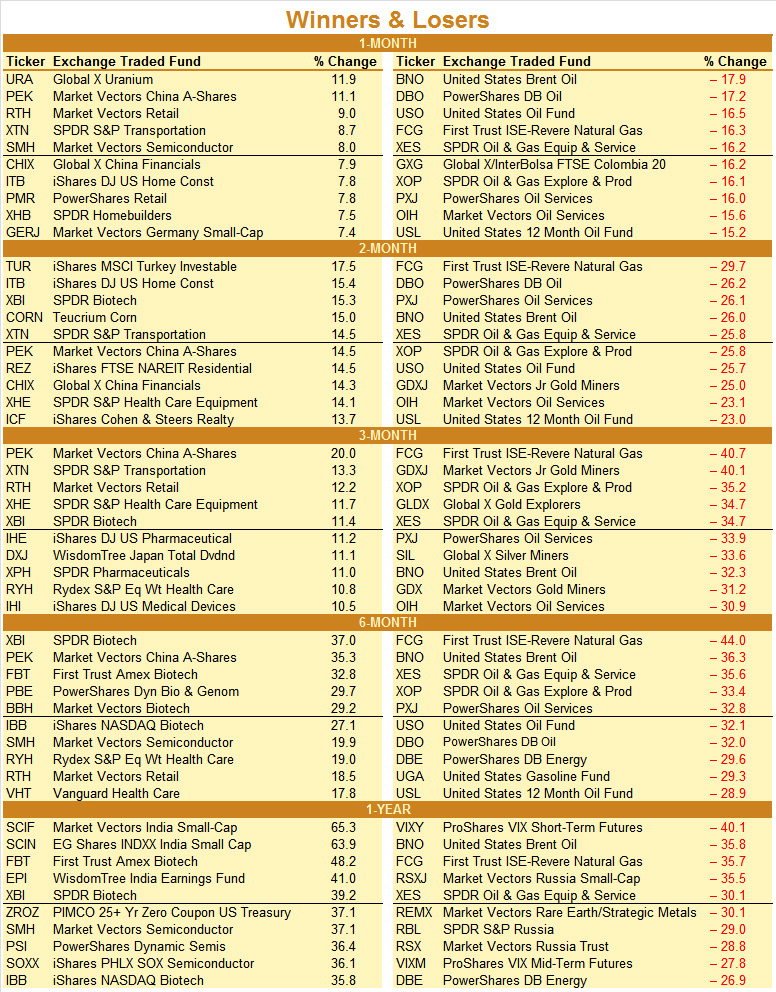

Gains were widespread across most ETF sectors last month with 22 of 29 advancing. The top five sectors were: Semiconductors (+6.7%), Software (+5.0%), Technology (+5.0%), Consumer (+4.9%) and Healthcare (+3.2%). Market Vectors Semiconductor (SMH) gained 8.0% in November, good enough for the fifth best, non-leveraged ETF performance in the 1-Month winners list. This gain was surpassed by SPDR S&P Transportation (XTN) up 8.7%, Market Vectors Retail (RTH) up 9.0%, Market Vectors China A-Shares (PEK) plus 11.1% and Global X Uranium (URA), climbing 11.9%.

Overall, the mix of China, Retail, Housing and Transportation related ETFs that rounded out the 1-Month winners list is an encouraging sign as all four represent substantial portions of U.S. and global growth, both actual and the apparently improving prospects for the future. A 7.4% advance by Market Vectors Germany Small-Cap (GERJ) is also notable as small-cap stocks tend to led following shifts in market sentiment and/or direction. Since Germany is widely recognized as the backbone of the European Union, any pickup in economic activity there is usually a positive indication for the rest of Europe.

Of the seven sectors that declined in November, Energy was the worst, off 8.7%.The majority of the declines were directly attributed to the decline in crude oil last month, especially on the last two days of November when OPEC did not trim production. United States Brent Oil (BNO) was the biggest loser, declining 17.9% in November and 35.8% over the past twelve months. As a result, all ten of the biggest 1-Month losers were either from the energy sector or directly related to crude. Global X MSCI Colombia (GXG) shed 16.2% as Columbia is a net exporter of crude and many of First Trust ISE-Revere Natural Gas (FCG) holdings are also directly exposed to the price crude oil. Crude oil remains seasonally weak through at least mid-December, but weakness can persist into February before a final low is reached.

New 52-Week Highs climbed modestly higher in November as major indices reached new highs while New 52-Week Lows shrunk slightly. Of the 281 New Highs, 250 were recorded during the last week of trading in November. Excluding Energy, Bear/Short and Natural Resources/Gold, New Highs were produced in all other sectors. New Lows were comprised mostly of gold and precious metals related funds early in November while later in the month, Energy and Bear/Short funds dominated. In short, this month’s ETF Scoreboard offers no evidence that the stock bull market is near its end yet.