December is the number one S&P 500 month and the second best month on the Dow Jones Industrials since 1950, averaging gains of 1.6% and 1.7% respectively. It’s also the top Russell 2000 (1979) month and second best for NASDAQ (1971) and Russell 1000. Rarely does the market fall precipitously in December. When it does it is usually a turning point in the market—near a top or bottom. If the market has experienced fantastic gains leading up to December, stocks can pullback.

Trading in December is holiday inspired and fueled by a buying bias throughout the month. However, the first part of the month tends to be weaker as tax-loss selling and yearend portfolio restructuring begins. Regardless, December is laden with market seasonality and important events.

Small caps tend to start to outperform larger caps near the middle of the month (early January Effect) and our “Free Lunch” strategy is served from the offerings of stocks making new 52-week lows on Triple-Witching Friday. An Almanac Investor Alert will be sent prior to the open on December 24 containing “Free Lunch” stock selections. The “Santa Claus Rally” begins on the open on Christmas Eve day and lasts until the second trading day of 2019. Average S&P 500 gains over this seven trading-day range since 1969 are a respectable 1.3%.

This is the first indicator for the market in the New Year. Years when the Santa Claus Rally (SCR) has failed to materialize are often flat or down. The last six times SCR (the last five trading days of the year and the first two trading days of the New Year) has not occurred were followed by three flat years (1994, 2004 and 2015) and two nasty bear markets (2000 and 2008) and a mild bear that ended in February 2016. As Yale Hirsch’s now famous line states, “If Santa Claus should fail to call, bears may come to Broad and Wall.”

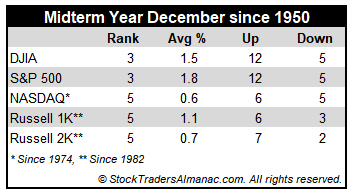

In the last seventeen midterm years, December’s rankings slip modestly to #3 S&P 500 (1.8%) and DJIA (1.5%) and #5 NASDAQ (0.6% since 1974). Small caps, measured by the Russell 2000, also perform well in midterm Decembers. Since 1982, the Russell 2000 has lost ground just twice in nine midterm years in December. The average small cap gain in all nine years is 0.7%. In 2010, Russell 2000 gained 7.8% in December.

December Triple Witching Week is more favorable to the S&P 500 with Monday up twelve of the last eighteen years while Triple-Witching Friday is up twenty-five of the last thirty-six years with an average 0.3% gain. The entire week has logged gains twenty-six times in the last thirty-four years. The week after December Triple Witching is the best of all weeks after Triple Witching for DJIA and is the only one with a clearly bullish bias, advancing in twenty-six of the last thirty-five years. However, three straight years of declines from 2006-2008 and 2012 have tempered its bullish bias. Small caps shine especially bright with a string of bullish days that runs from December 20 to 26.

Trading the day before and the day after Christmas is generally bullish across the board with the greatest gains coming from the day before (DJIA up eight of the last eleven). On the last trading day of the year, NASDAQ has been down in fifteen of the last eighteen years after having been up twenty-nine years in a row from 1971 to 1999. DJIA, S&P 500, and Russell 1000 have also been struggling recently and exhibit a bearish bias over the last twenty-one years. Russell 2000’s record very closely resembles NASDAQ, gains every year from 1979 to 1999 and only four advances since.

| December (1950-2017) |

| |

DJI |

SP500 |

NASDAQ |

Russell

1K |

Russell 2K |

| Rank |

|

2 |

|

1 |

|

2 |

|

2 |

|

1 |

| #

Up |

|

48 |

|

51 |

|

28 |

|

30 |

|

30 |

| #

Down |

|

20 |

|

17 |

|

19 |

|

9 |

|

9 |

| Average

% |

|

1.7 |

|

1.6 |

|

1.8 |

|

1.5 |

|

2.5 |

| 4-Year Presidential Election Cycle Performance

by % |

| Post-Election |

|

1.0 |

|

0.6 |

|

0.9 |

|

1.3 |

|

2.2 |

| Mid-Term |

|

1.5 |

|

1.8 |

|

0.6 |

|

1.1 |

|

1.7 |

| Pre-Election |

|

2.7 |

|

2.9 |

|

4.3 |

|

2.9 |

|

3.1 |

| Election |

|

1.4 |

|

1.2 |

|

1.4 |

|

0.8 |

|

3.0 |

| Best & Worst December by % |

| Best |

1991 |

9.5 |

1991 |

11.2 |

1999 |

22.0 |

1991 |

11.2 |

1999 |

11.2 |

| Worst |

2002 |

-6.2 |

2002 |

-6.0 |

2002 |

-9.7 |

2002 |

-5.8 |

2002 |

-5.7 |

| December Weeks by % |

| Best |

12/2/11 |

7.0 |

12/2/11 |

7.4 |

12/8/00 |

10.3 |

12/2/11 |

7.4 |

12/2/11 |

10.3 |

| Worst |

12/4/87 |

-7.5 |

12/6/74 |

-7.1 |

12/15/00 |

-9.1 |

12/4/87 |

-7.0 |

12/12/80 |

-6.5 |

| December Days by % |

| Best |

12/16/08 |

4.2 |

12/16/08 |

5.1 |

12/5/00 |

10.5 |

12/16/08 |

5.2 |

12/16/08 |

6.7 |

| Worst |

12/1/08 |

-7.7 |

12/1/08 |

-8.9 |

12/1/08 |

-9.0 |

12/1/08 |

-9.1 |

12/1/08 |

-11.9 |

| First Trading Day of Expiration Week: 1990-2017 |

| #Up-#Down |

|

17-11 |

|

16-12 |

|

14-14 |

|

16-12 |

|

13-15 |

| Streak |

|

U3 |

|

U1 |

|

U1 |

|

U1 |

|

D4 |

| Avg

% |

|

0.1 |

|

0.06 |

|

-0.03 |

|

0.03 |

|

-0.2 |

| Options Expiration Day: 1990-2017 |

| #Up-#Down |

|

17-11 |

|

19-9 |

|

18-10 |

|

19-9 |

|

16-12 |

| Streak |

|

U1 |

|

U1 |

|

U1 |

|

U1 |

|

U1 |

| Avg

% |

|

0.1 |

|

0.2 |

|

0.2 |

|

0.2 |

|

0.4 |

| Options Expiration Week: 1990-2017 |

| #Up-#Down |

|

22-6 |

|

21-7 |

|

18-10 |

|

20-8 |

|

16-12 |

| Streak |

|

U2 |

|

U1 |

|

U1 |

|

U1 |

|

U1 |

| Avg

% |

|

0.7 |

|

0.7 |

|

0.2 |

|

0.7 |

|

0.6 |

| Week After Options Expiration: 1990-2017 |

| #Up-#Down |

|

20-8 |

|

18-10 |

|

18-10 |

|

18-10 |

|

21-7 |

| Streak |

|

U5 |

|

U5 |

|

U5 |

|

U5 |

|

U5 |

| Avg

% |

|

0.8 |

|

0.6 |

|

0.8 |

|

0.7 |

|

1.0 |

| December 2018 Bullish Days: Data 1997-2017 |

| |

5,

17, 21, 26 |

5,

11, 17, 18 |

5,

6, 11, 21, 26 |

5,

11, 17, 18, 21 |

10, 18, 20, 21 |

| |

|

21,

26 |

|

26,-28 |

24, 26 |

| December 2018 Bearish Days: Data 1997-2017 |

| |

19,

31 |

31 |

19,

31 |

31 |

14, 31 |

| |

|

|

|

|

|